While Canadian western spruce pine fir’s (WSPF) production has decreased over the past decade, American southern yellow pine’s production has been on a steady rise, helping fill the void. In this article, we’ll delve deeper into these trends, the reasons behind them and their implications for buyers and producers of lumber in North America.

The decreased supply of WSPF can be attributed to several factors. Firstly, an infestation of bark beetles has affected the spruce trees in Western Canada, reducing production capacity. Also, wildfires have damaged forest stands and forced salvage harvesting, ultimately reducing the log availability over the longer-term horizon. Policy factors, including reduced harvest in old-growth forest stands in British Columbia, along with US Department of Commerce duties applied to Canadian lumber to US, have and will continue to be headwinds for future supply growth in the region.

Conversely, American southern yellow pine (SYP) has experienced steady growth in production over the past few years, advancing by over 10 billion board feet (bbf) since 2009 at the bottom of the housing crash and has continued to hit all-time records since 2019. SYP is mainly plantation grown in the southeastern US and is renowned for its strength and performance in treated applications.

The recent decline of western spruce-pine-fir

Recently, we’ve seen a major round of indefinite and permanent closures in British Columbia in response to weak market conditions, totaling 1.5 bbf over the last 12 months. On top of this, Fastmarkets’ wood products economists estimate that to date in 2023, over 1 bbf of temporary production cuts have been taken as mills look to rebalance an oversupplied lumber market, or equivalent to about 3% of domestic supply on an annualized basis.

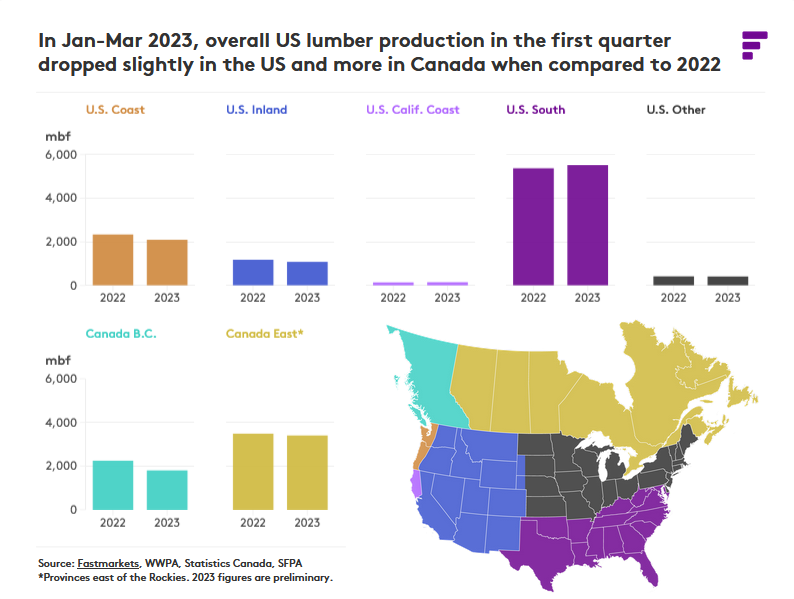

As reported in a recent edition of Random Lengths, overall production in North America through May 2023 totaled 24.22 billion board feet, a 4.9% drop from the same period of 2022. Output in the US fell 1.9% to 15.66 bbf, while the drop north of the border was more dramatic, as Canadian production fell 9.8% to 8.56bbf.

Hover over the chart below and use the arrow to click through this three-page data story.

Although overall production this year is unlikely to be positive given demand has fallen as a spike in interest rates drives housing demand downward, the situation is particularly gloomy in the British Columbia region. Lumber production is off by 17.7% (Jan-May year on year), far higher than any other producing region. Structural challenges with log supply and duties mentioned above have driven production costs to levels that have been particularly painful at current price levels as demand remains soft.

The recent supply reductions in British Columbia reflect longer-term secular trends in supply seen out of the region. When lumber market fundamentals weaken, we have and will continue to see continued rounds of supply reduction from the area as it copes with structural challenges that place it as the high-cost supplier of dimensional lumber in North America.

The future looks bright for southern yellow pine: short-term forecast

While the production cuts in British Columbia are a key headwind to the supply forecast over the coming years, supply growth in the US south is expected to help fill the void.

Contrary to the situation in British Columbia and Western US, the south has an overhang of timber supply, which is keeping production costs in the region competitive and returns for new mills investments very attractive. As a result, we are seeing a historical build-out in sawmill capacity in the region, which will continue to make its way into the North American and global marketplace.

Over the longer term, we anticipate more builders will substitute less readily available WSPF for SYP out of necessity, which will keep the overall lumber market competitive as SYP volume seeks a home in the marketplace. Meanwhile, fiber constraints in WSPF will be subject to further pricing volatility due to capacity closures in Canada, policy uncertainty and supply chain challenges as increasing wildfires and challenging winters disrupt shipping.

Over the coming years, we also predict the follow market developments:

- We forecast that the US South will continue to take a share of the total North American production mix over time.

- We expect the South’s share of US production to rise from 34% in 2018-22 to 39% from 2023-27 as demand grows and the South provides the only meaningful economical sources of incremental supply over the horizon.

- The South will see its share of North American offshore exports rise as it continues to be incorporated in new applications and Canadian supply becomes increasingly burdened by fiber constraints.