Across the country, many would-be homebuyers wait with bated breath for interest rates to make a meaningful drop before they either purchase their next home or their first house.

Persistently elevated rates have made it nearly impossible for lower-income mortgage applicants to qualify for financing. Meanwhile, those who purchased or refinanced a loan while record-low interest rates were available are staying put.

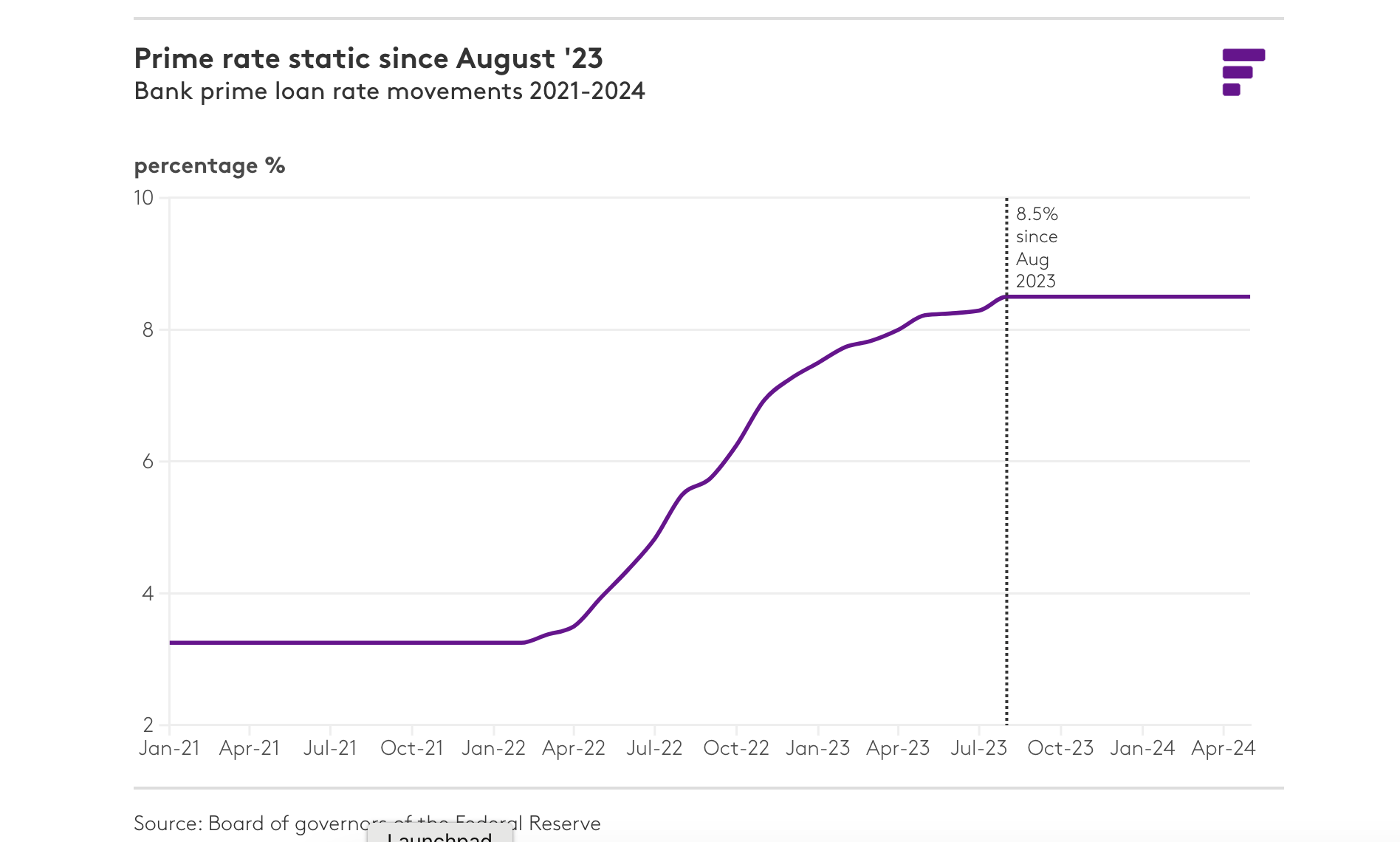

Federal Reserve Chairman Jerome Powell announced at the latest Fed meeting that they were not going to raise the federal funds rate, the upper limit of which has been at 5.50% for nearly a year. This means the rate cuts hoped for in June will have to wait until more progress is made on tamping down inflation. The prime rate, which moves in tandem with the federal funds rate, has been unchanged at 8.50% since August.

Just like those potential homebuyers waiting on the sidelines, the lumber industry is also anxious for rates to decline. “(Fed holding rates) has spurred a lot of negativity on the commercial and multifamily side. Buyers bought late last year and early this year anticipating better business, and they’re still sitting on those supplies, looking at the fourth quarter already,” said a Midwest distributor.

In a recently published National Association of Home Builders (NAHB) housing affordability report, nearly half of U.S. households were unable to afford a home exceeding $250,000. The data also revealed that 77% of Americans cannot afford the current median single-family home price of $495,750, at a mortgage interest rate of 6.5%.

This has led some cash-strapped buyers to purchase smaller homes. Median single-family floor area came in at 2,140 square feet, the lowest reading since the second half of 2009, according to first-quarter 2024 data from Census Quarterly Starts and Completions by Purpose and Design. Building smaller homes means less usage of framing lumber.

The one saving grace for wood demand has been the rebound in the single-family market…

“The one saving grace for wood demand has been the rebound in the single-family market. Low existing inventory and the ability of the larger home builders to offer rate buydowns are buttressing that segment of housing construction,” Coskren said.

Interest rates are not only hampering home purchasing, but money spent on home improvement as well. Current interest rate levels have “trapped” home equity as homeowners are reluctant to use a cash-out refinance or a home equity line of credit to finance home remodeling and repair projects. This is the case on both sides of the U.S.-Canada border.

The Leading Indicator of Remodeling Activity (LIRA) from the Joint Center of Housing Studies at Harvard University forecasts that annual spending for home improvements and repairs are projected to decline by 7% in the third quarter of 2024. However, they also expect that decline to soften by the first quarter of 2025.

Fastmarkets estimates that the repair and remodeling (R&R) market makes up more than 40% of softwood lumber demand in the U.S. “It’s a commonly known fact that the R&R volumes are significant when interest rates are neutral and employment is robust,” commented a Canadian distributor.

“In late 2023, most analysts had been calling for several interest rate cuts in 2024 as we saw inflation ease from its COVID peak. But inflation readings in February and March 2024 were running hotter than forecasted, with inflation ticking up. With consumer price gains holding stubbornly above the U.S. Federal Reserve’s target of 2.0%, the bond market has been less confident that several rate cuts will happen this year,” said, Jennifer Coskren, Fastmarkets senior economist.

April’s Consumer Price Index report showing an inflation growth of 0.3% offered a small glimmer of hope that inflation might be starting to ease from the levels reported in February and March. The Fed’s favored measure of inflation, the Personal Consumption Expenditures report, will be released on May 26. This report could give a clearer indication of when U.S. consumers can expect those long-awaited interest rate cuts to happen.

Source: Federal Reserve rate stagnation impacts wood products markets - Fastmarkets