By Brooks Mendell

This post is the second in a series related to the Q4 2022 Forisk Research Quarterly (FRQ), which includes forest industry analysis and timber price forecasts. This post includes excerpts from the featured research article by Nick Bolton, Brooks Mendell, and Shawn Baker on southern silviculture trends.*

Since 2012, Forisk has conducted biennial surveys of common forest management (silviculture) practices for private timberland owners and managers in the U.S. South (and has been doing the same in the Pacific Northwest since 2017). The six Southern surveys through 2022, which covered 24.6 million acres, are one of the largest datasets on private forest management and summarize a decade of silvicultural trends over a turbulent period in the U.S. economy and forest industry following the Great Recession.

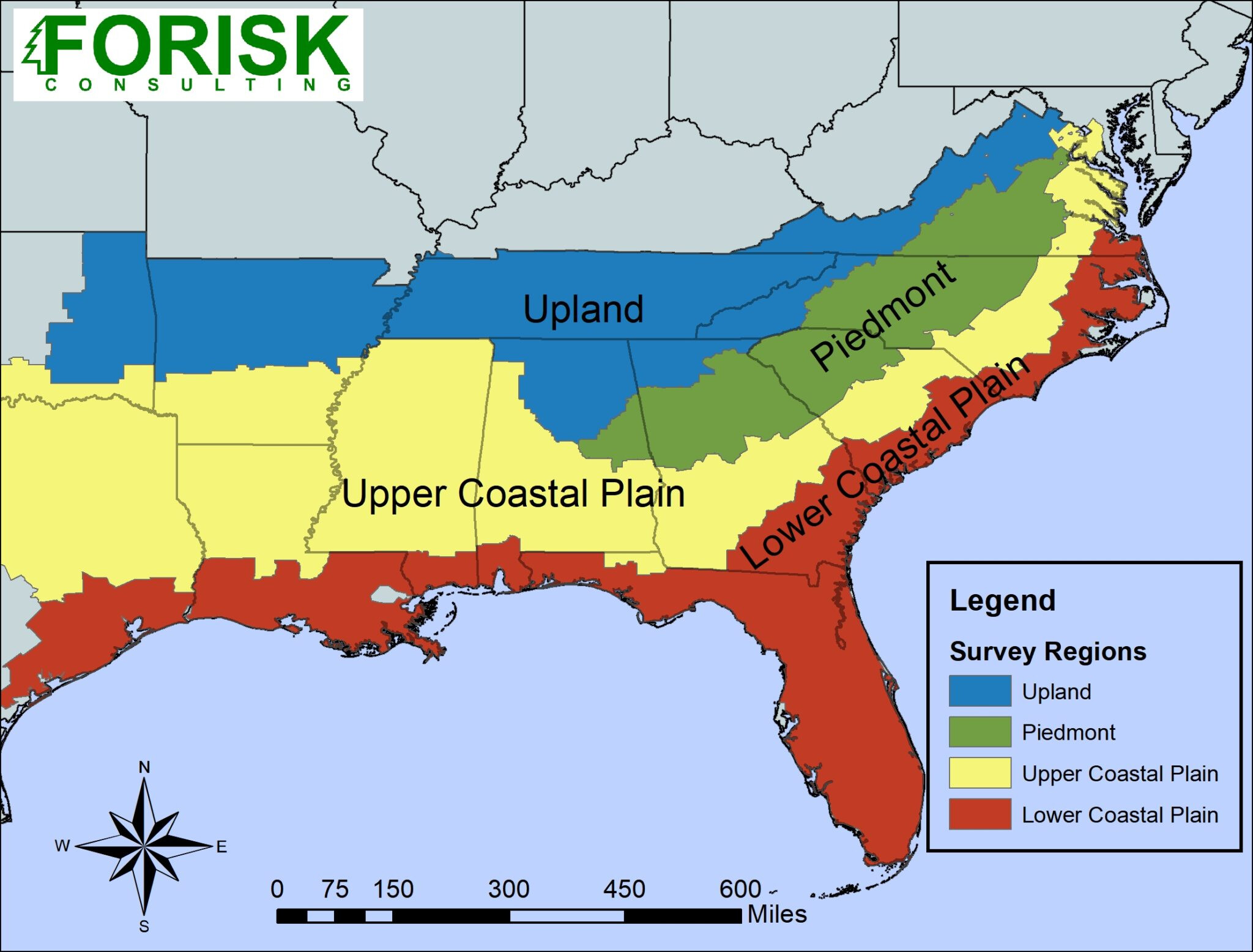

Forisk’s research tracks the intensity and variance in silvicultural activities across four physiographic regions in the U.S. South (Figure) to help participating forest owners and managers improve forest management decisions and benchmark performance. Survey participants include (1) TIMOs/Investment managers; (2) forest industry/REITs; (3) independent owners; and (4) forestry consultants. Most firms own and manage 10,000 timberland acres or more in the U.S. South, though a portion reported by consultants includes non-industrial private forest owners. The current surveys address 9 major topics:

Site preparation and regeneration

Competition control

Fertilization

Harvesting: thinning and final harvests

Site index

Property management, operational and tax costs (started in 2016)

Inventory management (started in 2016)

Forest certification

Other forest-related products and services

Figure: Physiographic Regions for Forisk’s Southern Silviculture Survey

Ten-Year Trends

One example of the trends covered in this research speaks to changes in regional trees per acre (TPA) planted, which have decreased over time from over 590 to under 570, as well as shifts in the types and percentages of acres planted in first generation, second generation, and controlled mass pollinated seedlings. Over the ten-year period, “other” seedling species accounted for less than 5% of the total planted area reported.

This research also reveals how long-term forest management is not immune to short-term economic activity. For example, the average age of clearcuts increased 4 years since 2012, from 29 years to 33, which counters one objective of intensive forest management (to grow more wood in less time). However, this variance from expectation is associated with deferred harvesting by timberland owners during and after the Great Recession. Also, our research finds that while actual average age at final harvest increased, the expected or managed age of trees planted has been stable. Specifically, timberland owners and managers expect to harvest the trees planted today at around 25 years of age, though this varies, as do the costs and specific activities, across physiographic regions.

Overall, trends in forest management practices across owner and manager types indicate that timberlands remain an attractive investment as real dollars still flow to managing and sustaining forests. The results also speak to the nuance across physiographic regions in the U.S. South with respect to practices, performance, and costs. As with timber markets, forest management reflects local conditions.