A slowdown in new household growth could ease prices and rents, but rising wages cause worry

The Federal Reserve’s interest rate increases have brought on a housing slump as severe, by some metrics, as that of 2007-09, inflicting pain on prospective buyers, homeowners, builders and other industries linked to real estate.

For the Fed, this is a feature, not a bug: Slumping housing could help deliver the lower economic activity and inflation that the Fed wants in the coming year.

The pandemic that hit the U.S. in March 2020 delivered an unexpected housing boom, driven by working from home, Americans’ desire for more space and the Fed’s slashing interest rates to near zero.

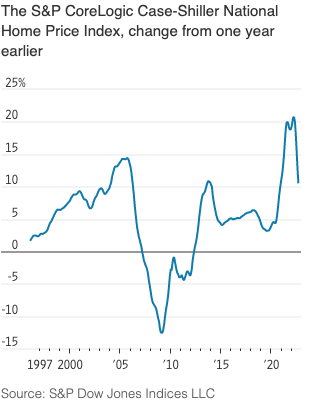

In the ensuing recovery, job growth fueled household formation as younger adults sought to live alone rather than with roommates or their parents. The result: Housing construction soared. The S&P CoreLogic Case-Shiller National Home Price Index leapt 45% from January 2020 to June 2022. Apartment rents also climbed sharply.

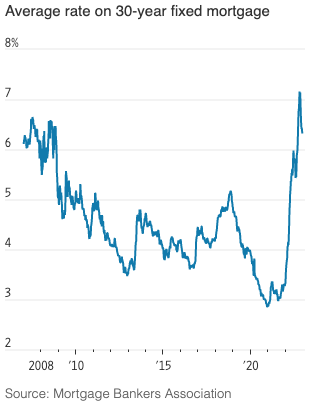

Caught off guard by the strength and persistence of inflation, the Fed reversed course in 2022, raising rates seven times to between 4.25% and 4.5% this month. The average 30-year fixed-rate mortgage jumped from around 4% in March to 7% this past fall. It recently eased back to 6.3%. The monthly mortgage payment on a home at the median U.S. price was up 43% in November from the start of the year, according to the Mortgage Bankers Association.

Higher interest rates check inflation by curbing spending, hiring and investment. The rate-sensitive housing sector is usually the first to feel this, but the speed and the severity this year has stunned longtime market participants.

“This is the worst rate shock I’ve ever seen by a mile,” said Lou Barnes, a third-generation mortgage banker in Boulder, Colo., who entered the lending business in 1978. He warned that the full effects have yet to be felt.

Buyers have retreated to the sidelines, while sellers who have locked in a low interest rate have less reason to sell.

Sales of existing homes fell in November for a record 10th straight month. Economists at Fannie Mae and Goldman Sachs forecast they will drop below 4 million in 2023, lower than during the 2006-11 housing bust.

Rent growth has also slowed as the household formation boom of the last two years appears to have ended and the supply of new apartment units hits a 40-year high.

Housing demand can grow because of increases in population or because new households are formed. Census Bureau information shows that the share of one-person households surged after the pandemic, likely reflecting behavioral changes as opposed to population growth, said Thomas Lawler, an independent housing economist in Leesburg, Va.

He estimated that if the share of households as a percentage of the population had been constant from 2021 to 2022, household growth would have been half as large as shown by Census Bureau figures.

If that surge proves to be a pandemic-related anomaly, household formation could be set for a bigger drop. “The cost to form a new household has gone up a whole lot,” said Mr. Lawler. “In my mind, it would be shocking if household growth actually hasn’t slowed dramatically.”

Typically, demand for rental housing rises in the late spring when college students graduate, but that didn’t happen this year, according to Jay Parsons, a housing economist at rental software company RealPage. “We’ve never seen a period like this, where we’ve had so much job growth, but so little demand for any type of housing,” he said. The demand unleashed by the pandemic “pulled forward” demand from the future, he said.

In November, single-family housing starts hit their lowest since the early months of the pandemic, while higher borrowing costs are chilling new apartment investment. “Anyone in the residential development business—for sale, for rent—is at a stop right now,” said Ric Campo, chief executive of Camden Property Trust, a Houston-based owner of 58,000 apartment units.

A housing slowdown could also crimp demand for appliances, renovations and moving services, among other businesses. Dan Neufeld, who runs Mt. Diablo Landscaping in Alexandria, Va., with his father, realized by June that the phone had stopped ringing. “We looked at each other and said, ‘My God, what’s happening? We should have way more estimates and appointments,’” said Mr. Neufeld.

He figures that the boom in patio installations that his company enjoyed during the Covid bubble—2020 and 2021 were two of his best years—brought forward sales that might have occurred in later years. “Right now, no one is pulling the trigger on a $20,000 or $30,000 patio renovation,” said Mr. Neufeld.

All this could have powerful effects on inflation.

Inflation was initially driven up by prices for such things as autos and furniture. Russia’s invasion of Ukraine this year further boosted prices for food, energy and other commodities.

Housing also contributed, with a lag, as rents and home prices soared. Housing accounts for a third of the consumer-price index and a sixth of the personal-consumption expenditures price index, which the Fed targets.

With housing prices now falling and rents growing much more slowly, shelter’s contribution to inflation could fall sharply in the coming year. It is one reason Fed officials project inflation will slow to 3.1% at the end of next year from around 6% now.

Fed officials aren’t sure that is enough to bring inflation durably down to their 2% target. They worry that growing incomes could sustain consumer spending in ways that allow companies to keep passing along higher prices.

Mr. Campo is sympathetic to Fed officials’ worry about wages. While Camden Property Trust’s share price has fallen 37% this year, the company is coming off one of its best-ever years, and his employees—with rising bills of their own—are expecting bigger pay raises.

“The pressure is on now: We’re going to raise wages more than we would normally,” he said. “You’re going to have a lot of wage pressure from companies that have to give more than the normal 3%. The question is, what is it—5%? 6%? 7%?”

By Nick Timiraos

Wall Street Journal

Dec. 25, 2022 5:30 am ET