The US housing market has had an uneven go of it in 2023, as mortgage rates rose dramatically, soaring past 7.0% in August. Affordability has worsened considerably, and the existing housing inventory continues to flirt with record lows. Demographics have contributed to this tight market, with millennials (those born between the early 1980s and mid-1990s), a cohort larger than the baby boomers, entering their prime home-buying years.

Many millennials have become homeowners, but a significant portion of them is still waiting to jump into the housing market. Not only are they facing tight inventory due to more homeowners keeping their ultra-low mortgage rates, but the competition for prime real estate has been exacerbated by continued buying by baby boomers. Mortgage rates are surging past 8.0%, dampening what had already been a challenging market to become a homeowner.

We know the challenges ahead for the housing market over the medium term, namely these higher borrowing costs. But the larger question looming is what do the demographics tell us about what we can expect longer term? Once we have these higher rates behind us, can we expect demographics to still be a strong tailwind? And an equally important question for market analysis is how truly under-built is the US housing market?

Long-term US population growth is revised downwards

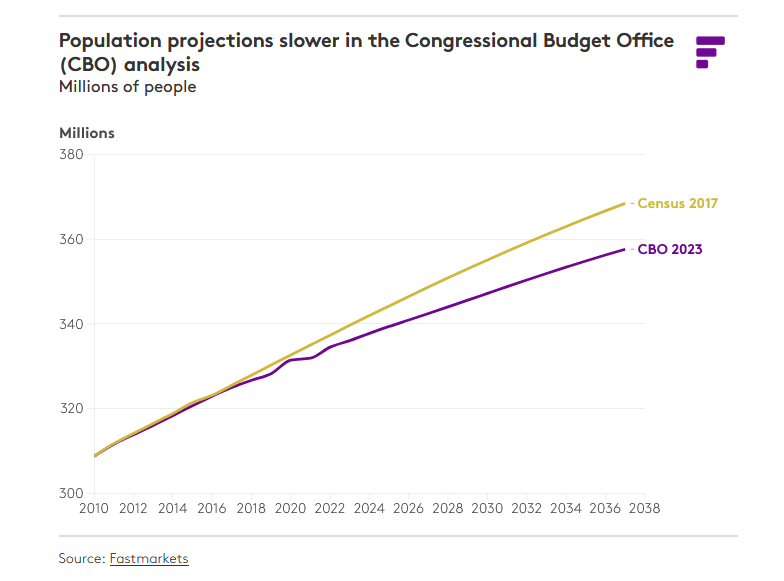

The Census has not been updated since 2017. Without updated Census numbers, Fastmarkets pivoted to another reputable data source for the nation’s long-term demographic profile. The Congressional Budget Office (CBO) released its latest estimates by age class in January 2023; its projections are lower than what the Census predicted in 2017. In 2037, the end of our forecast interval, the CBO currently projects the total US population will be 357.6 million, while the 2017 Census projected 368.4 million for that year — a difference of 11 million people (Figure 2). From 2023 to 2037, the CBO expects the US population to grow by about 0.4% per year, compared with the Census estimate of 0.6% per year, driven almost exclusively by immigration as birth rates will remain well below replacement rates over the forecast.

However, on the plus side, the CBO projections are more positive than what was released in July 2022, thanks primarily to higher immigration levels that are now tracking above pre-Covid-19 levels. According to the Migration Policy Institute, the US accepted 1 million immigrants as permanent residents in 2022, on par with pre-pandemic trends. Moreover, the State Department reported that it issued nearly 517,608 immigrant visas in FY22, over 50,000 more than in FY19. With one month left in FY23, the State Department issued another 588,611 immigrant visas, a 14% increase over the prior year.

Despite mortgage challenges, headship rates improve

Despite rapidly rising mortgage rates, household formations trended well above 1.0 million units in 2022 and continued to do so in the first two quarters of 2023. In 2022, households rose by 1.7 million units, with households that owned homes significantly outpacing those that rented. The headship rate ‒ which is defined as the number of total households divided by the population ‒ can be used to calculate a proxy for household size. But in a sign of how heated the housing market had become, those headship rates, while still low historically, have improved significantly. In 2022, the headship rate for the key demographic of 25-34-year-olds held at 44.6% compared with a low of 42.9% in 2017. The rate for 35-44-year-olds improved as well, rising to 51% in 2022 from a low of 49.2% in 2018. The improvement in the headship rate has been supportive of above-trend household growth despite the much slower population gains.

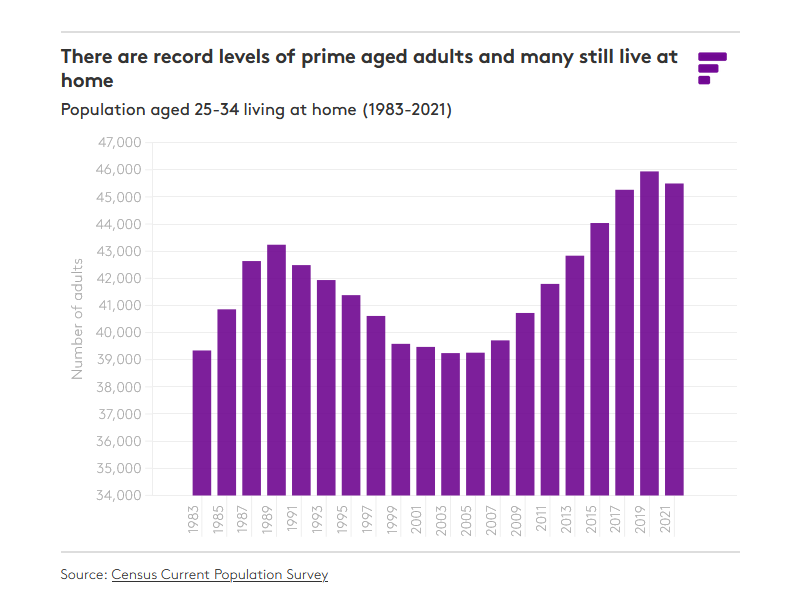

Headship rates could even be higher if not for the fact that the share of young adults living at home has been quite high, which is another element of the pent-up demand story. That share climbed after the Great Recession and has remained stubbornly high. The share hit a record level in 2020 as the pandemic ravaged the gig economy and hit young workers especially hard. The share dropped in 2022 and fell to 32.3%, slightly above the 2019 level of 31.6% but will remain high historically, partly due to affordability issues that are growing more acute (Figure 3). With the labor market holding up well in 2023, we expect the share of young adults living at home modestly fall again. But mortgage rates of over 7.0%, the resumption of student loan payments, high rental rates and general shelter affordability challenges will limit how much lower this share can go in the near term.

This share of young adults living at home has meant far fewer people in the shelter market than what the demographics would suggest. In a comparison of the headship rate of millennials to Generation Xers and baby boomers when they were 26-41 years old, Fannie Mae found that the headship rate of both boomers and Gen Xers was 53% at that age range. If millennials had formed households at the same rate as boomers and Gen Xers, the shelter market would have an additional 3 million households.

Large population increases are due to decline

Despite the lower headship rates and more young adults living at home, the sheer size of the millennial generation has been historic. But given current demographic projections, this surge in the population aged 25-34 is unlikely to continue. While the country will still have a high number of these prime-aged homebuying adults through the next few years, the large population increases are now in the rearview mirror. The average homebuying age is 31-32 years old. According to the US Census, between 2009 and 2019, over 5.2 million Americans entered the prime homebuying cohort of 25-34, but this age group will not continue to grow at such a fast clip in the next decade. While we have seen an upward revision to the latest CBO population growth projections, this massive demographic boost being over is still preserved.

Between 2022 and 2032, the population aged 25-34 will grow by 438,000 people to reach 46.4 million. Although this is an upward revision from -89,000 people in the 2022 CBO outlook, this is significantly slower than the millions recorded in the previous decade. Overall, the population in the next decade will grow more slowly, gaining about 15 million people from 2022 through 2032, compared with over 21 million people from 2009 to 2019.

While the 25-34 year olds will grow less robustly, the country will see continued gains for the 35-44 year old group. From 2009 to 2019, this age group basically trended sideways, averaging 41.7 million people in 2019, about where it was a decade before. But from 2022 through 2032, the age class will gain 3.3 million people. This age group is a bit older for first-time buyers, but it will likely mean more repeat buyers in the market potentially looking to trade-up from their first home.

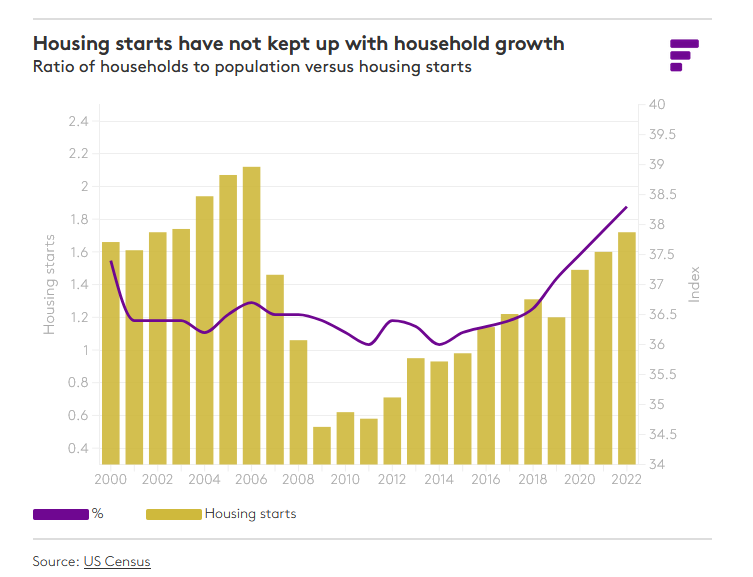

Although this outlook for population is less positive over the long term, the market has not been building enough homes in the last decade to meet the household growth the US has been experiencing. In particular, there have not been enough starter homes, and that has been worsening the affordability crisis of the last few years. But how under-built is the current shelter market? Assuming a target vacancy rate of about 12% (a more normal level of housing inventory) and a total headship rate of about 51%, Fastmarkets estimates that the market is currently under-built by about 2.0 million units. So, while we are expecting slower population growth, there is still an under-supplied element to the forecast that will be supportive of construction running above household formation trends in the medium term.