May 2023 Rental Report: Rents Start to Decline and the Trend is Expected to Continue

Jun 26, 2023

Jiayi Xu

Danielle Hale

Highlights

- May 2023 marks the first year-over-year rent decline for 0-2 bedroom properties (-0.5% Y/Y) observed since trend data began in 2020.

- The median asking rent in the 50 largest metros increased to $1,739, up by $3 from last month and down $38 from its July 2022 peak.

- Rent for 2-bedrooms saw its first year-over-year decline in our data history, while smaller units saw rents increase. Rent by size: Studio: $1,463, up 2.0% ($28) year-over-year; 1-bed: $1,628, up 0.4% ($6) year-over-year; 2-bed: $1,923, down 0.5% (-$10) year-over-year.

- Rents in the Midwest are slowing, but continue to increase (4.5% Y/Y), while rents in the West (-3.0% Y/Y) and South markets (-0.7%) were lower than a year ago.

- With the release of the mid-year forecast, we expect that the median asking rents will experience a small annual decline at a rate of -0.9% in 2023.

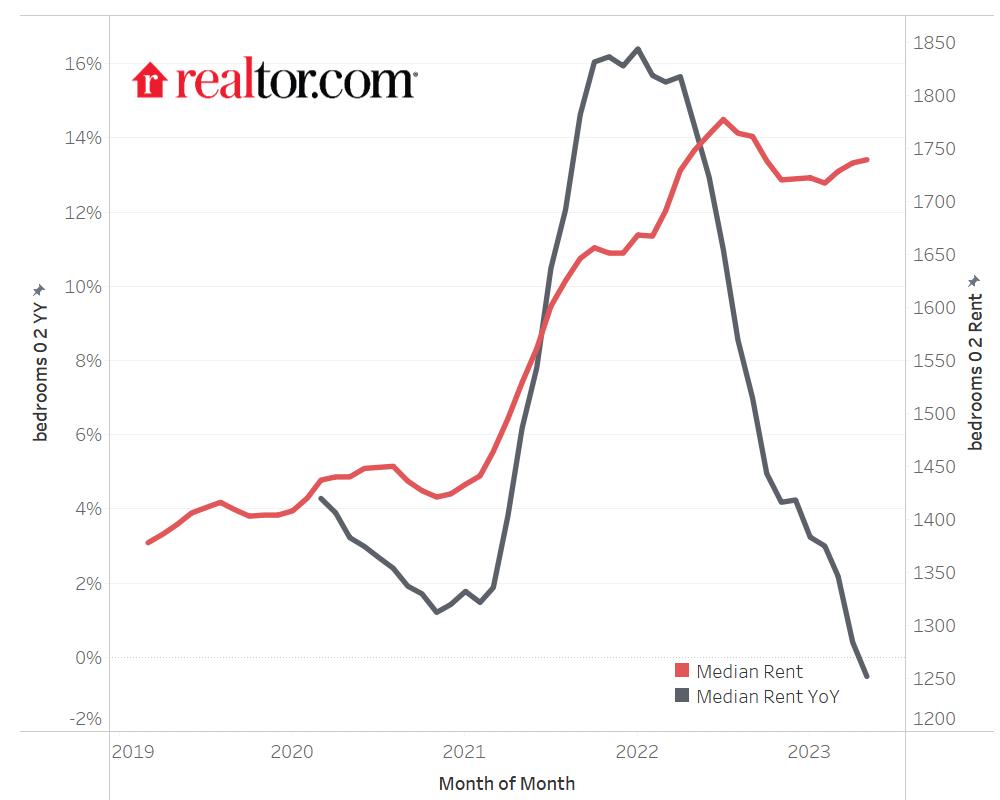

In May 2023, the U.S. rental market experienced its first year-over-year decline in our data history, down 0.5% for 0-2 bedroom properties across the top 50 metro.1 The median asking rent was $1,739, down by $38 from July 2022’s peak but still up by $3 from last month and $344 (24.7%) higher than the same time in 2019 (pre-pandemic).

The decline in rent will bring a sense of relief to renters who have been grappling with financial challengesthroughout the past years. In addition, as rent increases were more pronounced for new renters, many existing tenants chose to avoid higher costs by renewing their leases and staying where they are. As a result, the decline in rent prices may also be seen as a wake-up call for renters who have desired to explore regions abundant with job opportunities but have been hesitant to do so due to the excessively high move-in rental costs. In other words, if sustained, this shift in trend could potentially ignite an increase in renter mobility.

While the decline is something worth celebrating among renters, it is not completely bad news for landlords. Faster rent growth may have made it very challenging for landlords to find qualified tenants, increasing the risk of longer vacancies. Nevertheless, the decline in rents may impact landlords’ profit margins, particularly when considering the still-high inflation that may keep costs at elevated levels.

Figure 1: Year-over-Year Rent Trend

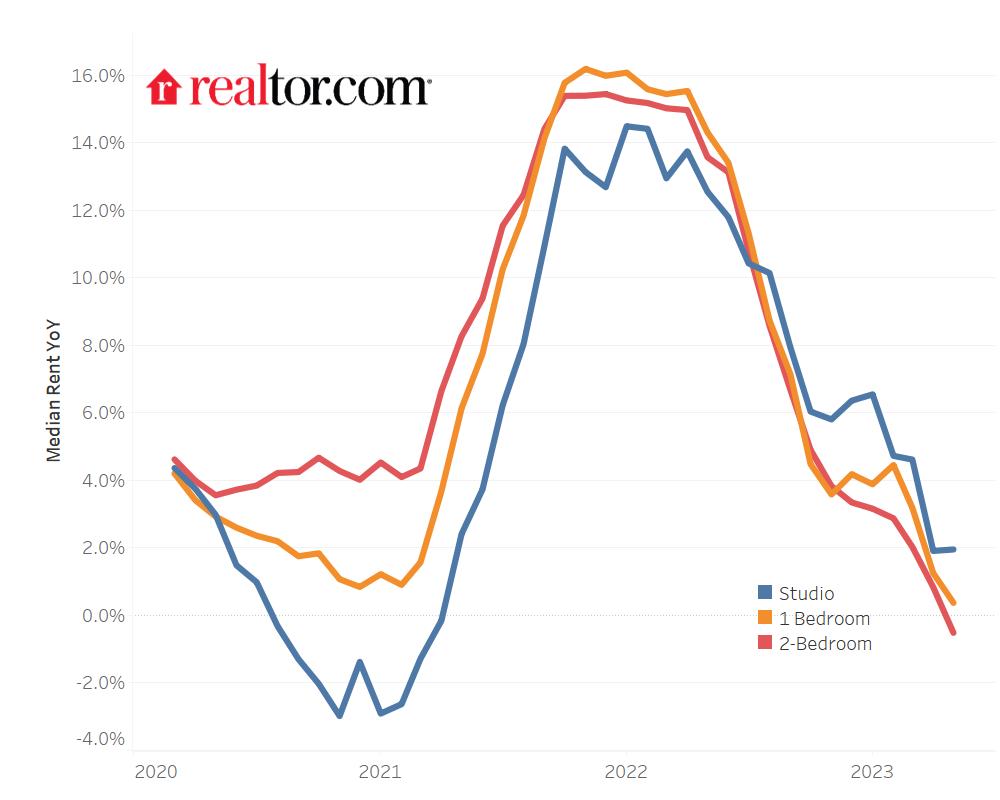

Two-Bedroom Units See First Rent Declines

In May 2023, the median asking rent for two bedroom units dropped 0.5%, marking the first decline in our data history (trends measured back to 2020). The median rent for two bedrooms was $1,923 nationally, $10 (-0.5%) lower than the same time last year and still $47 lower than the July 2022 peak. Nevertheless, the larger unit rents had the highest growth rate over the past four years, up by $417 (26.7%).

The rent growth for one-bedroom units on a year-over-year basis slided to 0.4% in May 2023, continuing the easing trend that began in March 2023. The median rent was $1,628, $6 higher than the same time last year and $337 (25.3%) higher since May 2019, but still $24 less than the July 2022 peak. .

In May, rent growth in studios was 2.0%. As renters sought affordability, studio rents have consistently outperformed larger 2-bedroom units over the last ten months. The median rent of studios was $1,463, up by $28 (2.0%) year-over-year and $262 (21.0%) higher than four years ago–a significant jump that is only slightly smaller than that seen in larger units. However, it is still $3 less than its peak seen in August 2022.

Figure 2: National Rent Trend by Unit Size

Table 1: National Rents by Unit Size

| Unit Size | Median Rent | Rent YoY | Rent Change – 4 years |

|---|---|---|---|

| Overall | $1,739 | -0.5% | 24.7% |

| Studio | $1,463 | 2.0% | 21.0% |

| 1-bed | $1,628 | 0.4% | 25.3% |

| 2-bed | $1,923 | -0.5% | 26.7% |

Rents in Western Metros Cooling Faster Than Their Northeast Peers

In May 2023, the median rent in the West was 3.0% lower than a year ago. San Jose, CA (1.0%) was the only large western metro seeing rent growth, but the growth rate was only one twentieth of what it was a year ago (19.3%). In contrast, rents in populous northeastern metros such as New York, NY (6.8%), Pittsburgh, PA (3.8%), and Boston, MA (3.3%)continued to experience faster growth.

One potential explanation for this discrepancy could be attributed to the robust labor market in the Northeast region. Over the past 12 months, the unemployment rate in the Northeast dropped from 3.5% to 2.8%. 2Although the unemployment rate in the West was similar to that of the Northeast in April 2022, standing at 3.4%, its labor market did not recover as strongly as its northeastern counterparts. As of April 2023, the West still experienced a relatively high unemployment rate of 3.4%. As a result, the stronger labor market in the Northeast may contribute to an increased demand for rentals, making it more competitive compared to the rental market in the West. In addition, the increase in the number of new rental supplies in the West could also dampen the competition. In the first quarter of 2023, non-single family homes were completed at an annual rate of 147,000 in the West, nearly doubling (84%) the pace in the same time last year.3 In contrast, the Northeast market saw non-single family homes completed at 60,000 units, a rate that was 40% higher than the same time last year, but a much slower growth than its western peers.

Rents in Midwest Markets Continue to See Faster Growth

Rents in Midwest metros continued to see faster rent growth. In May 2023, the median rent growth rate was 4.5%. As the Midwest markets tend to have greater affordability, the stronger growth in these markets likely results from this benefit even as it may reduce existing affordability. In addition, as the unemployment rate decreased from 3.2% to 2.8% over the past 12 months, the stronger job market could also boost the rental demand in this region. Among the top 10 metros experiencing the fastest year-over-year growth, six of them are located in the Midwest: Columbus, OH (9.3%), St. Louis, MO (7.7%), Cincinnati, OH (7.5%), Indianapolis, IN (7.3%), Milwaukee, WI (6.2%), and Detroit, MI (5.1%). The other four metros are Louisville/Jefferson, KY-IN (7.2%), New York, NY (6.8%), Richmond, VA (4.9%) and Oklahoma City, OK ( 4.6%).

Rents in South Markets Declined

In May 2023, the median asking-rent for 0-2 bedroom rental properties in the South was 0.7% lower than one year ago, despite a 0.2 percentage point drop in the unemployment rate. The top 5 metros experiencing the most significant year-over-year rent declines are: Austin, TX (-5.6%), Tampa, FL (-4%), Dallas, TX (-3.6%), Charlotte, NC (-3.5%) and Atlanta, GA (-3.1%). Interestingly, Austin, being recognized as one of the prominent tech hubs in the United States, similarly to its counterparts in the West, saw the most significant decrease in median asking rents compared to the previous year. In addition, as the tech sector in Tampa, Dallas, Charlotte and Atlanta all experienced significant growth during the pandemic, it is not surprising to find their rent trends closely resemble those of their western tech peers.

2023 Rental Market Forecast Update

With the release of the 2023 mid-year forecast, we expect that the rental price will drop -0.9% in 2023, a small annual decline in the median asking rents.

In the second half of 2023, the demand for rental properties is expected to remain strong. As housing prices and mortgage rates remain elevated, fewer renters are considering buying a home, and even those who still intend to become homeowners are postponing their home purchase and opting to stay in the rental market for a longer duration. However, the higher expenses associated with moving to a new residence in contrast to renewing a lease, along with the increasing gap in growth rates between rental prices for new tenants and lease renewals, create a strong incentive for existing tenants to remain in their current residences to save money. As a result, the lower mobility among renters is expected to dampen the level of competition within the rental market.

While we expect a small annual decline in rental prices, it is important to note that rent levels remain considerably high. Consequently, affordability remains a primary concern in the rental market. With renters actively seeking more affordable places to live, it is expected that lower-rent markets, particularly those in the Midwest region, will experience relatively stronger rental demand, leading to accelerated growth in rents.

On the supply side, the first quarter of 2023 witnessed a notable surge in newly completed multi-family units, surpassing the 450,000 mark. As a result, the rental vacancy rate experienced a significant increase in the first quarter of 2023, reaching 6.4%, the highest level observed in the past two years. However, even with a substantial increase in multi-family building that is expected to continue to push the vacancy rate higher, it is unlikely to bounce all the way back to the pre-pandemic level this year. If zero new households enter the rental market–well below our expectation, an additional 405,000 rental units is needed to push the vacancy rate back to 7.2%, the normal range from 2013 to 2019.

Nevertheless, the growing availability of rental options may pose challenges for property owners, as they may face difficulties in filling vacancies. In light of this market shift, a recent survey conducted by Avail highlighted that independent landlords are already adjusting their approach. Specifically, fewer independent landlords are planning to increase rents for lease renewals, indicating their awareness of the changing dynamics and the need to remain competitive in retaining existing tenants.