In 2021, Weyerhaeuser, the largest timberland manager in the United States, set a goal of achieving US$100 million of EBITDA from its Natural Climate Solutions business by 2025. This trajectory, seen as aggressive at the time, has since proved to be a key growth driver as Weyerhaeuser tracks to achieving this target.

Weyerhaeuser is perhaps the most prominent in a wave of US timberlands managers seeking to optimize financial performance from landholdings by complementing traditional forestry operations with forest carbon projects, conservation, renewable energy development, and subsurface leasing for carbon capture and storage (CCS) initiatives.

Over the last five years the forest carbon market in North America has experienced a period of rapid expansion, with a surge in dealmaking and heightened interest from institutional investors. In recent months, major corporations have signed high-profile offtake agreements for forest carbon credits, with the latest focus being on high quality-sequestration projects. At the same time, the uptake of Improved Forest Management (IFM) projects has grown, with over 1 million acres of IFM projects added in 2023 and 2024, reflecting the growing recognition of sustainable forestry as a viable tool for emissions removal and reduction.

The rise in corporate demand for nature-based solutions, coupled with compliance frameworks including California’s cap-and-trade and emerging cap-and-invest systems, are reshaping the market landscape. Investors, timberland managers, and carbon project developers are competing in an increasingly competitive and innovative space.

Understanding historical growth and value drivers

The United States holds the fourth largest area of forest cover globally and is a leading producer of forest products. Over the past two decades, the forest sector has undergone significant structural changes, particularly within the pulp and paper industry. While the US remains the world’s top producer of wood pulp, annual output has declined sharply – falling by 38% from a peak of nearly 60 million tonnes in 2000 to 37 million tonnes by 2024. This decline was driven by a combination of factors, including reduced demand from the graphic paper sector, aging and undercapitalized pulp mill infrastructure, and sluggish growth in markets such as containerboard and fluff pulp.

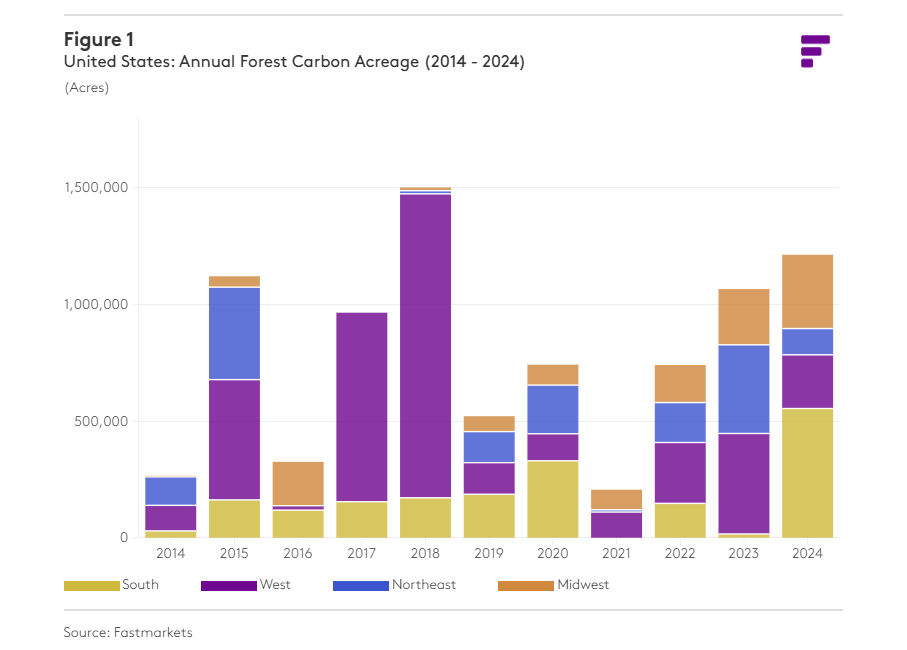

The steep decline in demand for pulpwood has forced timberland managers to look for additional sources of value to fill the gap left as their revenue streams shift, including the monetization of forest carbon. Forest carbon projects began to scale rapidly in the 2010s with increasing interest boosted by the development of the Californian cap-and-trade system, spurring the demand for carbon credits derived from the conservation and reestablishment of forests nationwide. By the end of 2024, cumulative forest carbon projects had grown to cover over 9.3 million acres across timberland areas in the United States.

Core to the growth of US forest carbon markets has been the expansion of Improved Forest Management (IFM) methodologies, which incentivize landowners to enhance carbon sequestration through sustainable forest management practices. By optimizing tree growth cycles, reducing harvest intensity, and extending rotation ages, IFM projects allow forests to store more carbon in comparison to conventional timber operations. This approach has been particularly attractive to managers who seek to diversify their revenue streams while keeping productive forests sourcing the traditional forest products markets.

Currently, IFM methodologies account for 86% of all the non-compliance forest-based credits issued in the country and are the primary source of credits tied to compliance systems. The remainder of that amount relates to credits issued under Afforestation, Reforestation and Revegetation (ARR) protocols.

The regional distribution of forest-based carbon projects across the United States varies widely, with Alaska and the West Coast historically accounting for most of the acreage enrolled in carbon initiatives. In recent years, however, the US South has emerged as a major growth region. Although this area holds the largest share of forest cover in the country, only about 0.7% of its forests are currently enrolled in carbon projects. Despite that small penetration, the South was responsible for 63% of all forest-based carbon credit issuances nationwide in 2024. This shift is particularly significant given that the region has been among the hardest hit by the decline in the pulp and paper industry. As a result, timberland managers in the South are increasingly turning to forest carbon as a value-added opportunity to diversify revenue streams and stabilize long-term returns.

(Full article here: Resilient growth in US forest carbon markets - Fastmarkets)