We live in chaotic times. Rapidly changing global events, from the pandemic to invasion and the splintering of energy and food markets, are reshaping the flow of goods and therefore the shape of supply chains.

As a leading provider of global supply chain intelligence, we have clients who ask us about the impact of current events on supply chains and transportation markets. The rapidity and severity of the sanctions that the international community has recently imposed on Russia provoked many questions about the effects on trade and supply chains.

We’ve already witnessed short-term volatility caused by the Russia-Ukraine conflict in the form of diesel fuel prices here in the United States and spiking container dwell times in ports like Rotterdam and Odessa. There is much more near-term chop ahead. But we think that the long-term effects of a persistent sanctions regime may end up being positive for North America.

In particular, the Russia-Ukraine conflict and Russia’s subsequent isolation from global trade under a severely restrictive sanctions regime may have some positive consequences for the U.S. economy. Like Russia, the U.S. is a major food and energy exporter. Rising prices in those commodities should stimulate domestic production and transportation as America backfills Russian supply and serves new markets.

But only if the conflict remains contained to Ukraine and doesn’t spill into a wider war. A wider war directly involving the militaries of multiple countries would greatly increase the human tragedy we’ve seen unfold in Ukraine. An escalation into a large conflict could shake global consumer confidence and destroy demand for freight. At present, we do not think the war is large enough to disrupt American consumers.

Anyone who has been around trucking for any length of time understands that hurricanes and other natural disasters drive substantial freight demand. These short-term demand surges create a demand for relief supplies to affected areas and rebuilding supplies after the disaster passes. Freight companies largely benefit from government-funded stimulus in the form of transportation demand for moving supplies to assist affected communities.

(Photo credit: U.S. Army)

I’ve known many trucking executives that secretly look forward to hurricane season for this reason. (Sorry; I don’t make the rules.)

Stimulating the freight economy

During a capacity-constrained part of the cycle, any increase in freight demand stimulates the freight economy. These demand surges create much higher spot rates as carriers respond to additional freight demand. While fuel prices also tend to rise, spot rates will rise much faster than fuel prices, and carriers will be able to absorb higher fuel prices due to higher trucking spot rates. For carriers that operate largely in the contract market, they are able to absorb fuel cost increases through fuel surcharges.

For the lucky carriers that operate in the contract market, fuel surcharges generate more revenue than they offset in fuel price increases. For many shippers, the fuel surcharge tables were designed when trucks averaged only 6 miles per gallon. What this means is that for every $.06/increase in fuel, the carrier generates $.01 per mile more in revenue. Newer trucks are pushing 9 miles per gallon, so while they are billing shippers an additional penny for every $.06/increase in fuel, their costs are only going up every $.09/mile.

In the past week, national truckstop retail fuel prices have jumped as much as $.70/gallon. For carriers that have such a fuel surcharge relationship, this could create $.11 more in revenue per mile, while the carriers pay $.07/mile. The $.04 per mile difference goes directly to the bottom line of the carriers.

The counter-argument I’ve heard among trucking executives about how fuel price spikes hurt truckers is the cash flow impact. While there is truth to this, many carriers factor their fuel or have the benefit of fuel advances that can help them pay for fuel immediately in return for a small fee or surcharge.

While all of the price action tends to play out within the first few months of a crisis, there are long-term implications at play as well.

Oil and agriculture

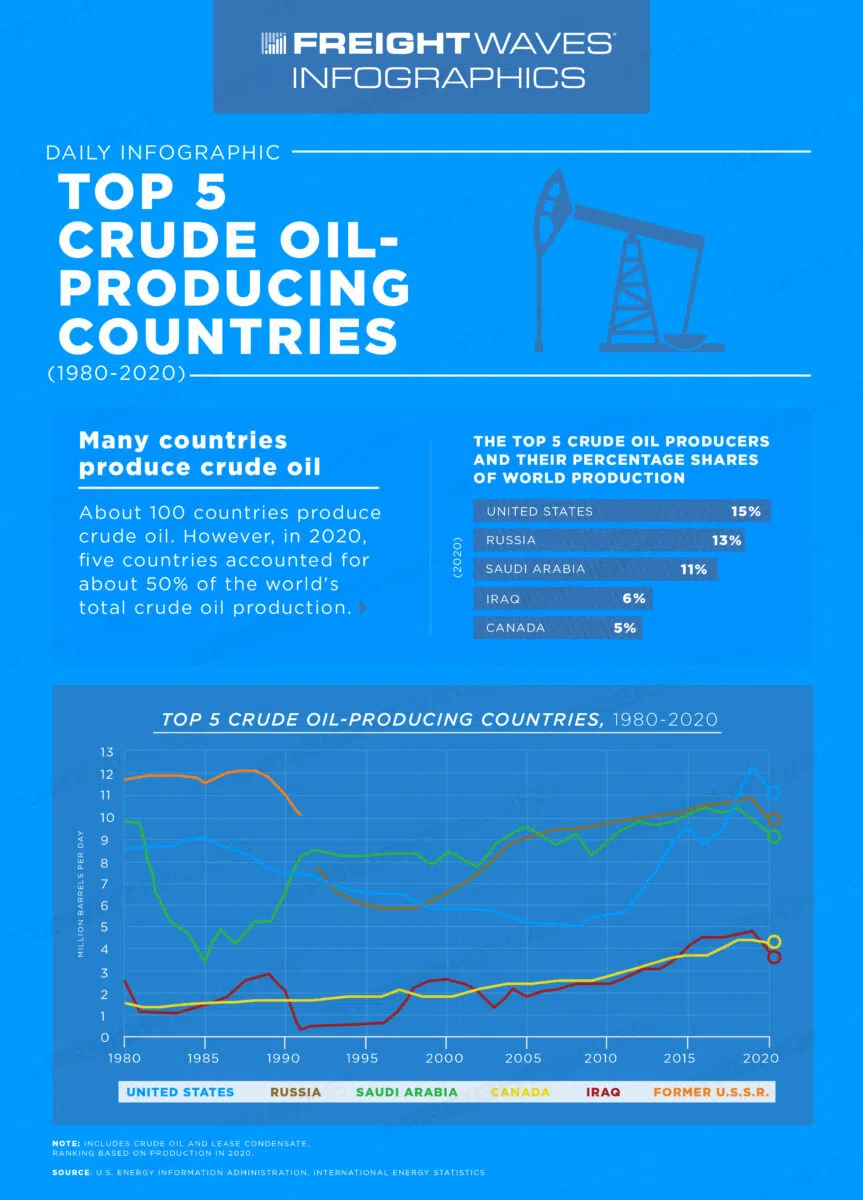

In regard to the Russia-Ukraine conflict, the U.S. freight economy will benefit over the long term. The United States competes with Russia on the global market in two key areas – energy and agriculture. The U.S. is the largest producer of oil in the world. In 2021, the United States produced 18.61 million barrels per day, far more than Saudi Arabia and Russia did individually. Saudi Arabia produced 10.8 million barrels daily, while Russia produced 10.5 million barrels daily.

Much higher oil prices over the past two weeks are a result of the world’s oil producers not being able to absorb the removal of much of Russia’s 10 million barrels of oil daily from the global market. In time, this circumstance will be corrected. The United States has the ability to produce more oil, but it will require additional investment to extract it. High prices will encourage investment in energy production, which drives freight demand in several ways – drilling site materials, oil production equipment and oil from wells.

In 2018, during the last big American shale boom, FreightWaves estimated that each new oil rig generates nearly one million truckload miles. As investment in drilling accelerates, there should be a net increase in domestic freight demand. Additionally, the United States leads the world in the manufacturing and design of energy-related equipment and technologies.

A wheat field in the Upper Midwest. (Image: Public Domain)

The U.S. is also the world leader in agricultural production and has a net export surplus. Ukraine is the breadbasket of Europe, supplying the continent with wheat and other dependable food supplies. With war disrupting the growing season and production of agricultural goods by Ukraine, Europe will look for reliable alternative sources.

The U.S. has a surplus of wheat and other grains to meet European demand and will benefit from much higher prices than before war broke out. According to Axios, wheat prices have jumped 70% in the past week alone. Agricultural goods ready for export will drive freight demand from farms in the heartland to ships bound for Europe. The higher prices and surge in demand will flow into U.S. farming communities, driving investment in the sector.

Increased defense spending

While no sane human wants war, it is a reality of the world we live in. The United States has the largest defense industry on the planet. For national security and international arms control reasons, the vast majority of American defense manufacturing and production takes place in this country. And many of the weapons and pieces of equipment being used in Ukraine were manufactured right here in America. A Lockheed Martin plant in Troy, Alabama, produces Javelin missiles; an Elbit Systems plant in Roanoke, Virginia, makes panoramic night vision goggles for the U.S. Army.

In recent weeks, European countries have woken up to the reality that their neighbors to the east threaten their security. Germany announced the biggest increase in defense spending since the 1980s, pledging to keep defense spending above 2% of GDP. (Additionally, American politicians will find great support for increased defense spending as the world comes to term with a Second Cold War.)

Logistics often determines the course of a war, with fuel, ammunition, food and water, and medical supplies needed on the front lines. (Photo: US Department of Defense)

The increased industrial production will mean a surge in freight demand. We’ve seen this before. The freight market in 2003-05 was one of the hottest in history, buoyed by domestic military and arms production caused by the wars in Afghanistan and Iraq. History will likely repeat itself.

Another byproduct of global tensions relates to inventory building and domestic sourcing. With global supply chains subject to disruptions due to global geopolitical tensions, companies will look for production sources closer to home. This will benefit places like Mexico, but also will mean companies will seek to build up inventories. Inflation also means that products and inventories become worth more as time goes on, offsetting potential downsides in holding inventory that would otherwise exist in a low inflation environment.

Anything that is manufactured in North America will certainly benefit the American freight market, as transportation services will be involved in all stages of supply chain sourcing, production, assembly and distribution. When companies source and manufacturer products in China, much of the freight spend would remain in that region, far away from American logistics companies.

The threat of global military conflict is something that few in the freight industry would ever hope for. But the world we live in is becoming more contested than it has been in 80 years. With that comes a great deal of pressure on our freight and logistics networks.

Anyone that has studied military conflict can attest that supply chains and logistics win wars and the United States has the most sophisticated logistics networks in the world – and that it is ready for almost anything.