Key takeaways:

- Low-grade lumber prices are surging due to mill capacity losses and advanced optimization technologies.

- Rising diesel fuel costs and shrinking trucking capacity add major freight expenses to pallet production.

- The Gulf Coast chemical sector faces heavy exposure to these escalating regional pallet and logistics costs.

- Chemical procurement teams must proactively manage regional pallet sourcing and ensure sufficient ISPM-15 export inventory.

Prices for low-grade lumber – the main input cost for pallets – have moved sharply higher since the start of 2026, and the Iran conflict is now adding a second layer of pressure through fuel and freight. In this viewpoint, we look at what is driving the run-up in pallet lumber prices, why the low-grade market has tightened faster than framing lumber, and how higher diesel and tighter trucking conditions could compound those costs in the months ahead. We also spotlight the chemical industry, where Gulf Coast producers are especially exposed to this combination of rising pallet input costs and worsening transportation expenses.

Why are low-grade lumber prices shrinking the grade gap?

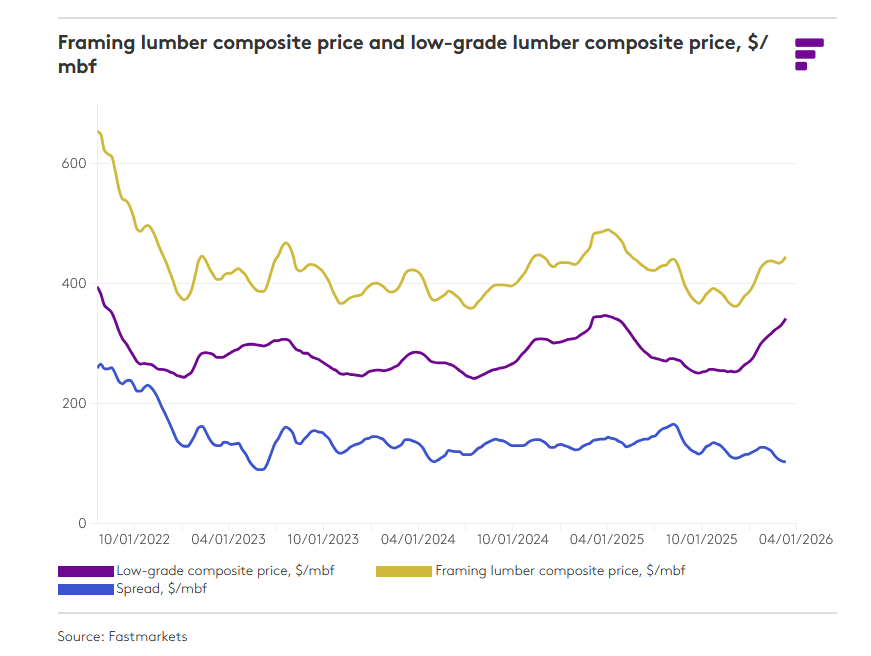

The first sign of this tightening is the shrinking gap between low-grade and framing lumber prices. Since the first week of January, our low-grade lumber composite price (LGLCP)index has risen 27%, compared with a 14% increase in the framing lumber composite price (FLCP). That has pushed the spread between the two to its narrowest point since May 2024.

Notably, #4 grade lumber has been driving most of these gains. In Southern Yellow Pine markets, #4 grade posted the largest gains, with 2×4 in the Westside market rising 41% since early January and 2×6 seeing a 46% increase in the same Westside market. This isn’t isolated to Southern Yellow Pine, with similar dynamics emerging in western species as well. #3 Hem-fir and Douglas-fir have risen by just over 30%, while hem-fir #4 2×4 rose by 65%, and fir-larch #4 2×4 rose by 53% since early January.

Supply of industrial lumber has been tightening for structural reasons. Modern softwood mills, particularly across the Southeast, have invested heavily in scanning, optimization systems, and newer profiler heads that remove wane before the first cut scan. The effect is greater recovery of higher-grade boards and less low-grade lumber making its way into pallet markets. At the same time, mill curtailments and permanent closures have reduced the amount of lumber available overall. Fastmarkets estimates that 775 MMBF of capacity was lost in 2025 through indefinite and permanent closures, following an even larger 3,665 MMBF reduction in 2024. Canadian duties, fiber constraints, and the aftereffects of SYP oversupply have all contributed to a smaller and more volatile supply base.

As #4 lumber becomes harder to source, buyers are pushed up the grade stack into #3 and, in some cases, even #2. That substitution effect is important because it spreads inflation through the pallet lumber basket rather than leaving it isolated in the lowest grades. By late February, that pressure had already started to show up in the pallet market. Producers who had struggled to pass through higher costs in January found more room to raise quotes as February progressed, helped by reduced pallet production, leaner field inventories, a tighter core market, and continued inflation in low-grade inputs.

The next risk is that freight will start amplifying the lumber story, particularly with the fallout from the Iran conflict. Trucking employment has been steadily falling since late 2022, after the significant ramp up after the pandemic caused freight rates to fall drastically as there was too much competition.

How do rising diesel rates impact the lumber supply chain?

This slow shedding of trucking availability suggests the industry is already operating with thinner capacity and weaker margins. Now diesel prices are rising sharply as geopolitical tensions in Iran lift energy costs. According to the EIA, the national average diesel price for the week ending March 23 reached $5.375 per gallon, up $1.808 from a year earlier and about 40% from a month earlier. That raises delivered lumber costs, squeezes already thin trucking margins, and increases the risk of further carrier exits. For pallet buyers, that means additional cost pressure through more expensive low-grade lumber at the mill and a more expensive trip getting it to market.

Further upstream in the pallet supply chain lie more challenges. For loggers, diesel is not just another cost, but something that could destroy their already tight margins. With product prices still weak and little room to pass higher costs along, a sustained rise in diesel increases the odds of logging cutbacks, setting the stage for tighter log supply in the second half of 2026 should the increase in diesel prices be prolonged.